The Alkali Manufacturers Association of India (AMAI) is instead in luck because it represents the pursuits of a homogenous industry manufacturing chlor-alkali products

Caustic soda, chlorine and soda ash in the main, not like other industry association that represents a extensive cross-section of the chemical industry. The challenges and the treatments are common throughout the membership of AMAI, and it could put them across to the powers that be in a coordinated manner with little warfare throughout its member base. In some chemical enterprise segments – agrochemicals and pharmaceuticals come immediately to mind – there are numerous foyer agencies that declare to talk for subsets of the industry and the messaging that comes throughout from them is frequently at cross-purposes, confusing policy makers.

To the credit score of AMAI, it has also consistently been doing an amazing job of documenting the performance of the industry, and the modern day handbook launched by the association, placing out the industry overall performance in FY24, follows at the tradition of many years. Some factors that stand out within the latest record is the multiplied potential utilization of the caustic soda manufacturing industry as a whole thanks to higher exports; better chlorine utilization largely through captive utilization; and a drop in capability utilization in the soda ash industry – the other segment of the alkali industry – thanks to stiff competition from imports.

Caustic soda

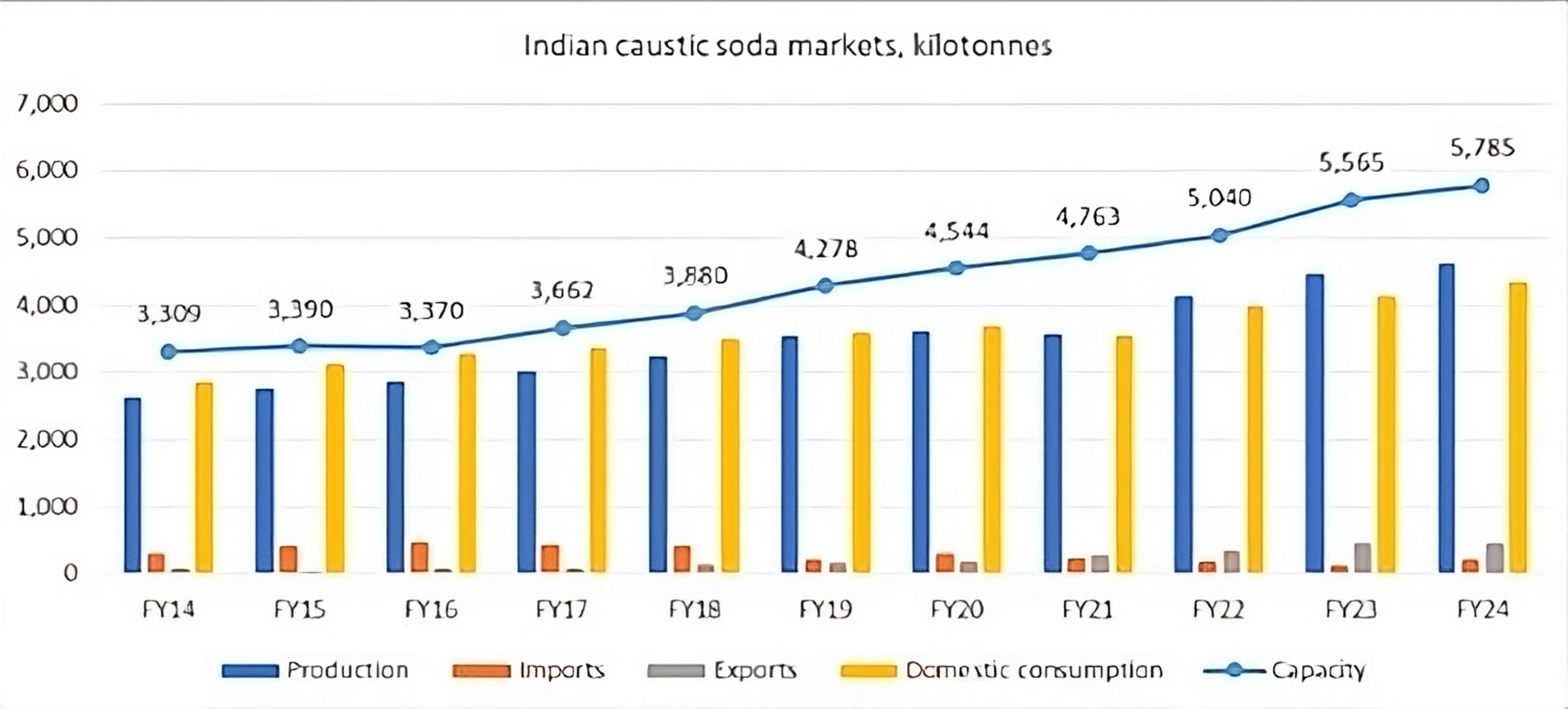

The Indian chlor-alkali industry is still small in a international context, with an installed capacity of 58.85 ltpa (lakh tonnes per annum) for caustic soda, representing just 5.5% proportion of world manufacturing potential. The industry has visible a fixed increase in capacity – rising by using a CAGR of 6.2% among FY20 and FY24, as numerous players elevated capacities. In FY24, manufacturing increased through 3.1% over the previous year to 46.13-lt. Capacity utilisation of the industry as a whole rose to 81.6%, as compared to 80.3% in the preceding year, way to extended exports (extra on this later) and growth in domestic demand. The industry has traditionally run at an operating rate in the low to mid 80s, however this plummeted in FY21 to 75.3% largely because of COVID-associated effects. But, like many different segments of the chemical industry, the caustic soda industry acted a quick healing and went lower back to trendline operating rates within the next years.

Much of the industry is focused in Gujarat, which has a 57% share of total opened capacity, not surprising viewing about the place is a primary producer of salt (the main raw material for both caustic soda and soda ash), and the products find ready use in the commercial units in the region. The State additionally keeps to see expansions and new ventures by way of incumbents. South India (mainly Andhra Pradesh) has the second one biggest cluster of caustic soda production units and noticed an 8.9% growth in capacity in FY24 to take its percentage of overall established capacity in the country to about 20%.

Caustic soda is a globally traded commodity, especially within the form of lye, and cheap imports were a hazard. The industry has traditionally been a net importer, but that changed in FY21, when it turned a small net exporter – a status that has been maintained. Imports have fallen in current years in part due the bulky logistics involved in ferrying a cheap commodity; the imposition of protect and antidumping responsibilities; and growing manufacturing. From accounting for approximately 18% of intake in FY16, imports are now only a notch above 5% (mostly lye), which can be nicely accommodated by raising domestic manufacturing within the capacity already existing.

For numerous years, Japan has been the number one source of caustic soda to India, and in FY24 accounted for 41% of all imports. That any such high-value country account for a big percentage in a commodity like caustic soda appears surprising, however the purpose has to do with the Indo-Japan Free Trade Agreement (FTA), beneath which, the Basic Customs Duty (BCD) on imports of caustic soda is ‘Zero’. Prior to the signing of this accord, Japan’s percentage become subsequent to not anything. Iran and Oman within the Middle East are different great suppliers to India. Their ability to compete may be attributed to their geographical proximity and low energy costs, which makes for attractive procedure economics. Total value of caustic soda imports in FY24 become approximately Rs. 775-crore.

At the identical time, exports have grown, and in FY24 reached near half of million tonnes – more or less about 10% of production. Industry contributors believes this momentum in exports may be built upon, furnished the right policy guide is drawing close to cope with shortcomings in the industry’s price structure. Much of the exports are the solid form (not the commonly traded lye), which has a restricted market however nonetheless has enough headspace to permit growth. Much of the exports are to lesser advanced markets; in FY24 the pinnacle locations for Indian caustic soda exports were South Africa, Indonesia, Kenya, Tanzania, Saudi Arabia and Nigeria, observed by way of several other African countries. Total value of exports was approximately Rs. 1,600 crore.

The pattern of consumption of caustic soda in India has some similarities with the world as an entire, as well as a few stark differences. The single largest outlet in both is alumina production from bauxite, which share in India is about 16% and in the global approximately 21%. The project here stock from the reality that almost all of this demand is in the eastern parts of India, at the same time as much of the caustic soda capability is in the west. If future alumina capability expansions aren’t matched by means of needful caustic soda capability, it’s going to want lugging of the chemical (with 67% water) lengthy distances – hardly ever an efficient plan.

The share of intake in the pulp & paper industry – which is the second biggest outlet globally with a 16% share – is simply 5.5% here. A similar percentage of consumption is seen for making a slew of organic & inorganic chemical, as well as in soaps & detergents.

Chlorine

Chorine output is continually in a fixed proportion to caustic soda (1.1 tonnes of caustic soda according to tonne of chlorine) and the assignment for the industry here has been getting a reasonable price for the halogen. An analysis of the present day consumption pattern for chlorine famous that as much as 18% of output went to make hydrochloric acid (HCl). Though HCl does have numerous makes use of, together with in anhydrous form, it normally represents low value addition to chlorine, and is, at instances, more a way of converting chlorine to a portable form. About 16% of chlorine is now ending up each in chloromethanes and chlorinated paraffin wax, and in the former there is a danger of overbuild of potential considering about call for for methylene chloride, mainly, will now not maintain as much as the increasing trends of the past (lots of its use is as solvent in the pharmaceuticals industry, which emissions are possibly to be curbed).

Only approximately 8% of total chlorine demand in India is within the vinyl industry – for making ethylene dichloride (EDC), which is then converted to vinyl chloride monomer (VCM), before being polymerised into polyvinyl chloride (PVC) resin, for which India has reputedly insatiable appetite. This is in sharp contrast to the global pattern of intake wherein vinyls account for approximately a third of the chlorine consumed. The irony here is that India is the world’s largest importer of PVC resin – with annual imports in FY24 reaching 26.18 lt – representing 64% of domestic demand.

In latest instances new capacities for epichlorohydrin, chlorinated PVC (CPVC), calcium chloride, etc. Have arise, and rather eased the industry’s assignment of having reasonable price for the chlorine co-produced. Importantly, about 2.45 mtpa of latest PVC resin production ability is anticipated by way of 2028 – 1.2 mtpa from Reliance Industries Ltd., 1 mtpa with the aid of the Adani Group, and 0.25 mtpa via Indian Oil Corporation with captive manufacturing of caustic soda/chlorine. Investments also are being planned in extra propylene oxide (PO) and CPVC capacity (India is now the world’s largest market for this polymer, which has sizeable use in plumbing), and there’s some hypothesis that a ventures for MDI is also inside the offing.

All of those developments are welcome, however there may be a threat that the chlorine utilization problem that has historically plagued the Indian chlor-alkali enterprise might also grow to be a caustic soda one, until a further upward thrust in exports of the alkali can come to the rescue.

{kind=link}